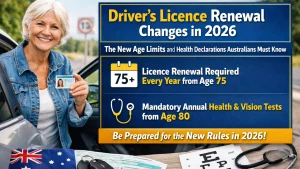

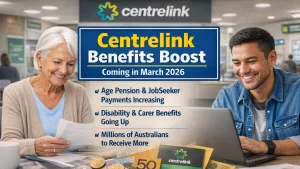

For many retired Australians, the fortnightly pension payment is a crucial source of financial stability. As the cost of groceries, utilities, and healthcare continues to rise, small changes in pension payments can make a meaningful difference to household budgets.

In March 2026, Australia’s pension system is expected to deliver updated payment rates following the regular indexation process. The adjustment could mean higher fortnightly payments for eligible couples receiving the Age Pension. These updates are designed to help pensioners keep up with changes in the cost of living and inflation.

Here’s what retirees and couples receiving the pension need to know about the March 2026 update.

What’s Changing in the March 2026 Pension Update

Australia adjusts Age Pension payments twice each year, typically in March and September, to reflect economic indicators such as inflation and wage growth.

The March 2026 adjustment could result in higher payments for couples who receive the full pension rate.

Key points about the update include:

- Potential increase in fortnightly Age Pension payments

- Adjusted income and asset test thresholds

- Continued indexation based on inflation and wage benchmarks

- Higher combined payments for eligible couples

These changes aim to ensure pension payments maintain their value as living costs increase.

New Estimated Fortnightly Pension Rates for Couples

While final figures depend on official indexation calculations, projected increases suggest that couples receiving the full pension may see a modest boost to their fortnightly payments.

Below is an example of how the updated payment levels may compare.

| Pension Type | Previous Rate (Approx.) | Estimated March 2026 Rate |

|---|---|---|

| Single Pensioner | $1,116 per fortnight | Around $1,140 per fortnight |

| Couple (combined) | $1,682 per fortnight | Around $1,720 per fortnight |

| Each Partner in Couple | $841 per fortnight | Around $860 per fortnight |

These estimates include the base pension, pension supplement, and energy supplement that many pensioners receive.

Actual payment amounts will depend on individual circumstances, including income, assets, and eligibility.

Why Pension Payments Increase

The Age Pension is indexed to ensure it keeps pace with economic conditions. The government reviews pension rates twice each year to maintain purchasing power for retirees.

The indexation formula generally considers:

- Consumer Price Index (CPI) – measures inflation

- Pensioner and Beneficiary Living Cost Index (PBLCI) – tracks living costs for pensioners

- Average weekly earnings benchmarks

If living costs rise, pension payments are adjusted to reflect those increases.

These adjustments are particularly important for retirees who rely primarily on the Age Pension as their main source of income.

Who Is Eligible for the Age Pension

To receive the Age Pension in Australia, individuals must meet several eligibility requirements.

Key criteria include:

Age Requirement

Applicants must be 67 years or older, which is the current Age Pension eligibility age.

Residency Requirement

Applicants generally must:

- Be an Australian resident

- Have lived in Australia for at least 10 years, with five of those years continuous

Income Test

Pension payments are reduced if income exceeds certain limits. Income sources that may be assessed include:

- Employment income

- Investment earnings

- Rental income

- Superannuation income streams

Assets Test

Assets such as property (excluding the family home), savings, and investments may also affect pension eligibility.

If income or assets exceed certain thresholds, pension payments may be reduced or stopped.

Comparison: Previous vs March 2026 Pension Rates

| Category | Previous Fortnightly Payment | Estimated March 2026 Payment |

|---|---|---|

| Single Pensioner | $1,116 | Around $1,140 |

| Couple (each) | $841 | Around $860 |

| Couple (combined) | $1,682 | Around $1,720 |

| Pension Supplement (couple combined) | Included | Included |

| Energy Supplement | Included | Included |

These figures represent estimated maximum rates before income or asset reductions.

How Indexation Works

Pension indexation occurs automatically and does not require pensioners to submit a new application.

During the indexation review, government agencies analyze economic indicators and determine whether payment adjustments are needed.

The process typically includes:

- Reviewing inflation data

- Comparing pension payments with wage benchmarks

- Calculating new payment levels

- Applying the updated rates automatically to eligible recipients

Once the new rates are approved, updated payments usually begin in the weeks following the March indexation announcement.

What You Should Know

If you or your partner receive the Age Pension, the March 2026 update could result in higher fortnightly payments.

Important points to remember:

- Pension increases happen automatically after indexation

- Couples may receive higher combined payments

- Payment increases depend on eligibility and financial circumstances

- Income and asset thresholds may also be adjusted

To ensure payments remain accurate, pensioners should keep their financial information updated with the relevant government agency.

Q&A: March 2026 Pension Increase for Couples

1. When will the pension increase take effect?

The updated rates are expected to apply after the March 2026 indexation review.

2. Do pensioners need to apply for the increase?

No. Pension increases from indexation are applied automatically.

3. How much could couples receive after the increase?

Eligible couples could receive around $1,720 combined per fortnight if receiving the full pension.

4. Will singles also receive a payment increase?

Yes. Single pensioners may also receive higher fortnightly payments after indexation.

5. Why does the pension increase twice a year?

The government adjusts payments to reflect inflation and living costs.

6. What determines the size of the increase?

Economic indicators such as CPI, wage growth, and pensioner living cost indexes.

7. Could income affect the payment amount?

Yes. Income above certain thresholds may reduce pension payments.

8. Do assets affect pension eligibility?

Yes. Savings, investments, and property (excluding the family home) are assessed.

9. Will supplements increase as well?

Pension supplements and energy supplements are usually included in the updated payment calculations.

10. Can pension payments decrease?

Typically, indexation increases payments, but personal income or asset changes could reduce eligibility.

11. What should pensioners do before the update?

Ensure financial and personal details are up to date with the government.

12. Are couples paid more than singles?

Yes. Couples receive a combined payment that is higher than the single pension rate.

13. How often are pension rates reviewed?

Twice each year — in March and September.

14. Will the payment increase cover rising living costs?

Indexation aims to help pensions keep pace with inflation.

15. Where can pensioners see updated payment amounts?

Updated payment details will appear in official pension statements once the changes are applied.

Leave a Comment